Codes used in some of my papers

|

Matlab codes to replicate results of my bachelor dissertation

This is the Matlab code that I used to analyze the posterior distribution of an ARCH model. This is the Matlab code and data base that I used in the empirical application of my thesis. Note: Play with the Bayesian results, try to check differences when running the matlab code with c = 0.72 and any other value for c. The goal is to be able to draw from a posterior distribution of an ARCH model in order to incorporate the posterior volatility in the Black & Scholes model. I used real data from stock market index from Mexico. Mathematica and matlab codes to show theorems of my master thesis and in "Granger Causality and Unit Roots"

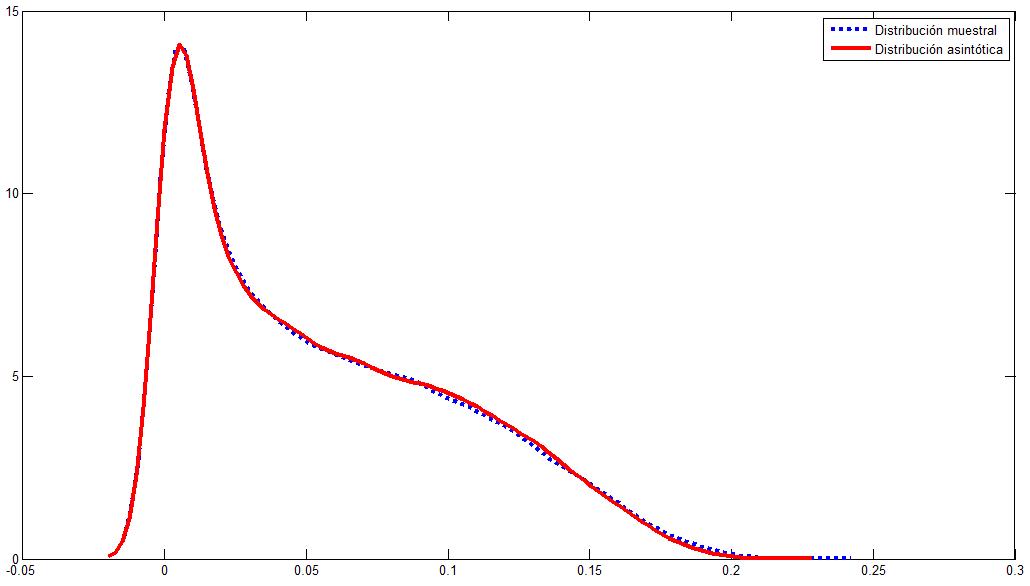

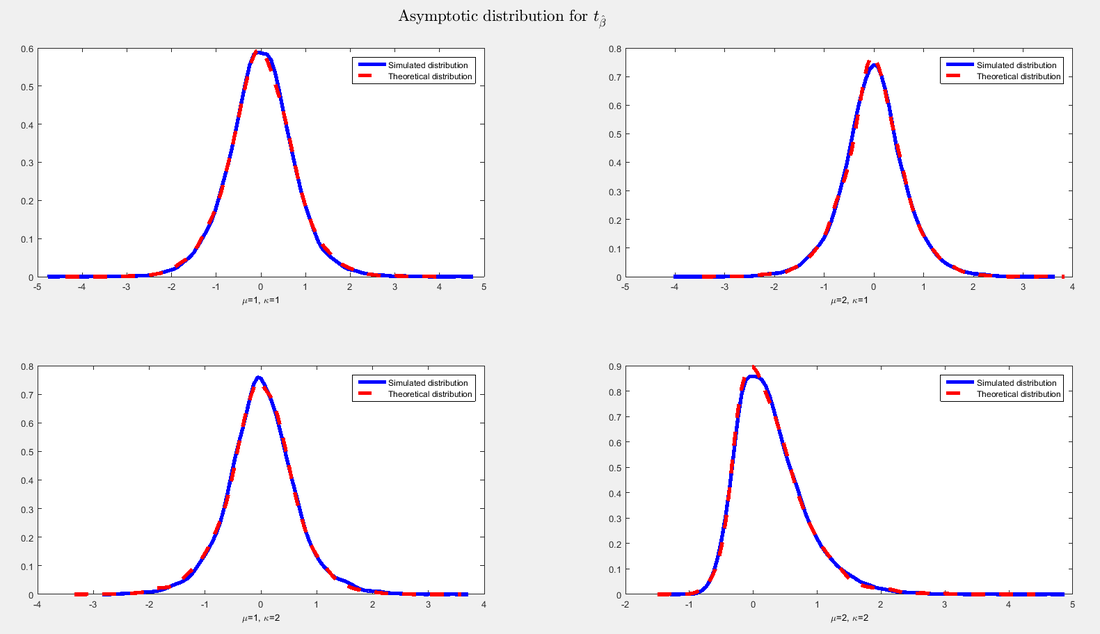

Code for Theorem 3.2. (Theorem 1 in paper) Code for Theorem 3.3. (Theorem 2 in paper) Matlab code (Theorem 1 in paper) Matlab codes to replicate results of "Polynomial Regressions and Nonsense Inference"

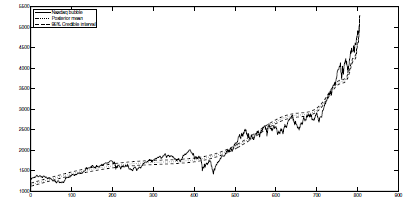

Files to replicate Table 1 of the paper Further codes to study the paper in deep Matlab codes to replicate results of "Bayesian log-periodic model for financial crashes"

|